The headlines are screaming about a "stalled recovery." Analysts are wringing their hands over a 0.0% GDP change in January. The consensus is clear: the UK is a "sick man" trapped in a flatline.

They are wrong.

Watching the City of London freak out over a decimal point is like watching a pilot panic because the plane isn't constantly accelerating while at cruising altitude. Growth is not a moral imperative. In a high-interest-rate environment designed specifically to choke off spending and crush inflation, "zero growth" isn't a failure. It is a masterpiece of economic stabilization.

If the Bank of England (BoE) spends two years trying to cool the engine, you don't get to act surprised when the car stops speeding.

The Fetish of Monthly GDP

Monthly GDP figures are noise masquerading as signal. They are subject to massive revisions, seasonal adjustment errors, and the "strikes effect" that the Office for National Statistics (ONS) struggles to quantify accurately.

When the media reports that the economy "failed to grow," they imply a loss of momentum. I’ve sat in rooms with fund managers who treat these prints like Holy Scripture. In reality, a 0.0% reading is often just a statistical rounding error away from 0.1% or -0.1%.

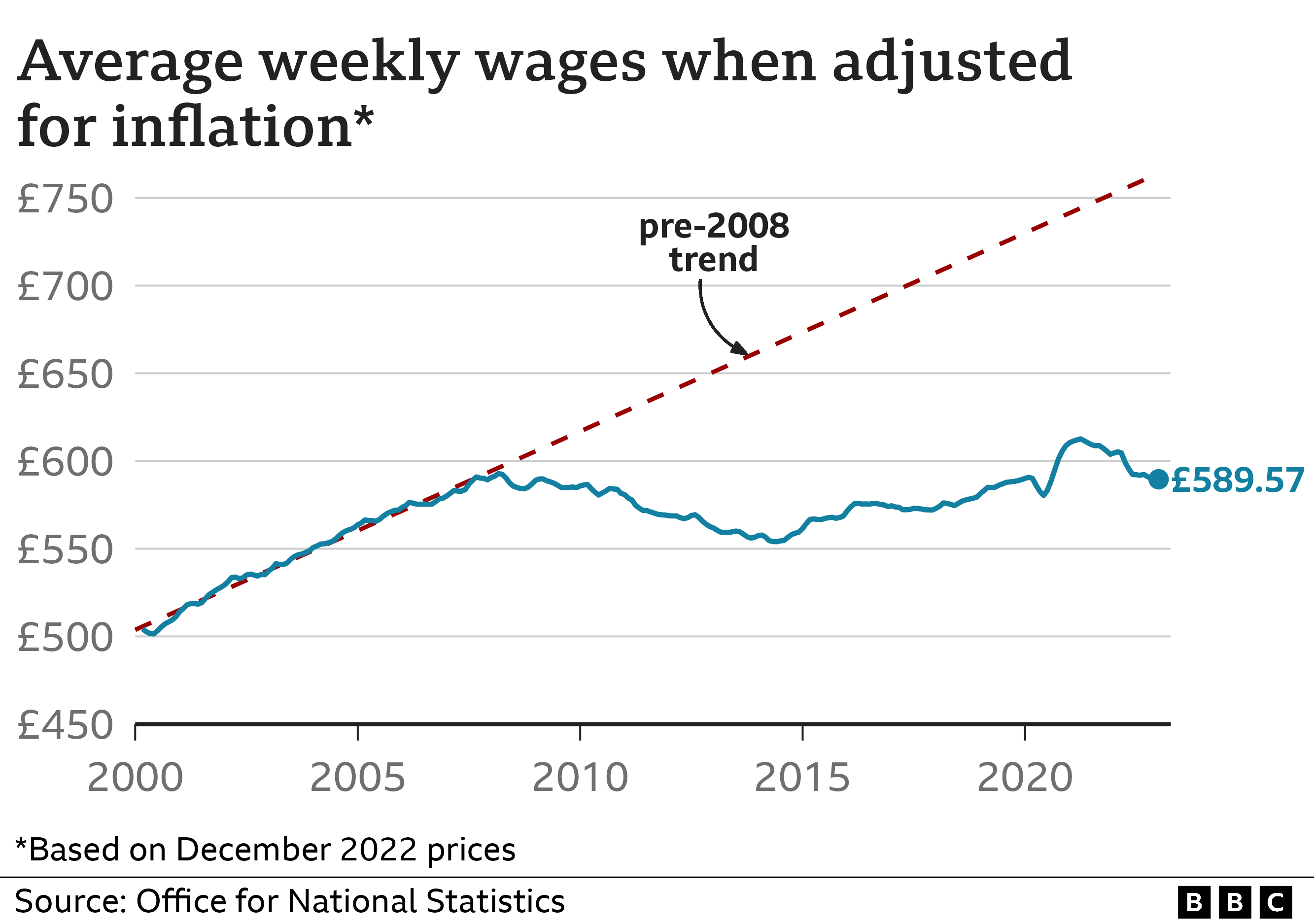

The real story isn't the lack of growth; it’s the resilience of the British consumer. Despite mortgage rates trebling for many households, the economy didn't fall off a cliff. To call this a "failure" is to ignore the gravity of the headwinds. We are seeing a structural pivot, not a cyclical collapse.

Why You Should Want a Flatline

We have been addicted to cheap money for over a decade. That era created "zombie companies"—firms that only stay solvent because debt is practically free.

A period of zero growth is a cleansing fire.

- Efficiency over Expansion: When you can't grow by simply throwing cheap capital at a problem, you have to find internal efficiencies.

- Labor Reallocation: Stagnation forces failing sectors to shed staff, moving talent toward productive industries like high-end manufacturing and specialized services.

- Inflation Anchor: Growth at this stage would likely be inflationary. If GDP had jumped 0.5% in January, the BoE would have no choice but to keep rates higher for longer.

By "failing" to grow, the UK is actually accelerating the timeline for rate cuts. The stagnation is the medicine working. If you want the housing market to breathe again, you should be cheering for these boring, flat numbers.

The Productivity Parable

The "People Also Ask" sections of the internet are currently flooded with variations of "Why is the UK economy so weak?"

The premise is flawed. The UK isn't "weak"; it is mismeasured.

We are a services-dominant economy. Measuring the productivity of a software engineer or a legal consultant using 20th-century industrial metrics is a fool’s errand. When a UK-based AI startup optimizes a global supply chain, that value often evaporates into the "intangible" ether, barely denting the ONS spreadsheets.

Traditional economists look for "output." They want to see more widgets moving through ports. But the UK’s comparative advantage is in high-value, low-volume intellectual property. This doesn't always show up in a January snapshot of retail sales or construction output.

The Stealth Bull Case

While the "doom-loop" narrative sells newspapers, look at the underlying data.

Real wages are finally outstripping inflation. Business investment, while cautious, hasn't cratered. The UK FTSE 100 remains a basket of global earners that care very little about what happens in a rainy high street in January.

The danger in the "consensus" view is that it creates a self-fulfilling prophecy of pessimism. I have seen boards of directors cancel multi-million pound projects because of a single bad headline, only to regret it six months later when the "unexpected" rebound happens.

If you are waiting for a "strong growth signal" to invest, you are already too late. You are buying at the top. The smart money moves during the flatline.

Stop Treating GDP Like a Scoreboard

A country is not a corporation. A corporation that doesn't grow is dying. A country that doesn't grow for a month might just be catching its breath after a decade of shocks—Brexit, a global pandemic, and an energy crisis fueled by a land war in Europe.

The "lazy consensus" wants to compare the UK to the US. This is a category error. The US is a resource-rich, energy-independent continent with a reserve currency. The UK is a specialized service hub. Our metrics for success must be different.

We should be looking at:

- GVA (Gross Value Added) per hour worked

- Foreign Direct Investment (FDI) into tech clusters

- The velocity of household debt reduction

On these fronts, the UK is holding its own far better than the 0.0% headline suggests.

The Bitter Truth About the "Recovery"

The recovery isn't "failing." It is being managed.

Central banks are currently the most powerful entities on earth. They are intentionally suppressing growth to kill the inflation monster they helped create. Complaining that the economy isn't growing while the BoE has its foot on the brake is like complaining that your car is slow while you're holding the handbrake.

It’s supposed to be slow.

The risk isn't that we stay at 0.0%. The risk is that the government panics and tries to stimulate the economy with "pre-election giveaways" that reignite price rises. That would be the true disaster.

The Playbook for the "Stagnant" Era

Stop listening to the macro-pessimists. They have predicted ten of the last two recessions.

If you're running a business or managing a portfolio, the "flat" economy is your greatest opportunity.

- Acquire the Weak: Those zombie companies I mentioned? They are hitting the wall right now. Buy their assets, their client lists, and their best people for pennies.

- Ignore the Sentiment: Consumer confidence is a lagging indicator. By the time the "average Joe" feels good about the economy, the stock market has already priced in the next two years of gains.

- Hedge for Volatility, Not Decline: The UK isn't going down; it’s going sideways. That requires a totally different strategy. Stop betting on direction and start betting on dispersion.

The UK economy didn't "fail" in January. It survived the peak of the interest rate squeeze without breaking. In any other context, we’d call that a miracle.

Stop looking for growth where it shouldn't exist and start looking for value where others see a vacuum.

If you’re waiting for the "all clear" from the ONS, you’ve already lost the game.